Ghana Priorities: Agriculture

Technical Report

This paper had a simple aim. It sought to estimate the magnitude, relative returns, and economic viability of selected interventions in agriculture in Ghana.

The five interventions studied were selected because they were implicitly consistent with government’s plans to increase agriculture growth and use that as a launching pad for the country’s industrialisation plans. The interventions analysed included fertilizer subsidies, increased mechanisation (essentially more use of tractors), improved seeds subsidies, increased irrigation schemes, and more warehouses to help reduce post-harvest losses.

The analysis was done for each of the interventions as a stand-alone and there was no attempt to test for complementarities. Since this was a cost-benefit analysis of the different interventions we identified and estimated the cost elements first. Typically, this was made up of some fixed as well as variable costs. The second element, the benefits stream, was essentially the monetised value of incremental output due to the respective interventions – output with intervention less output without intervention.

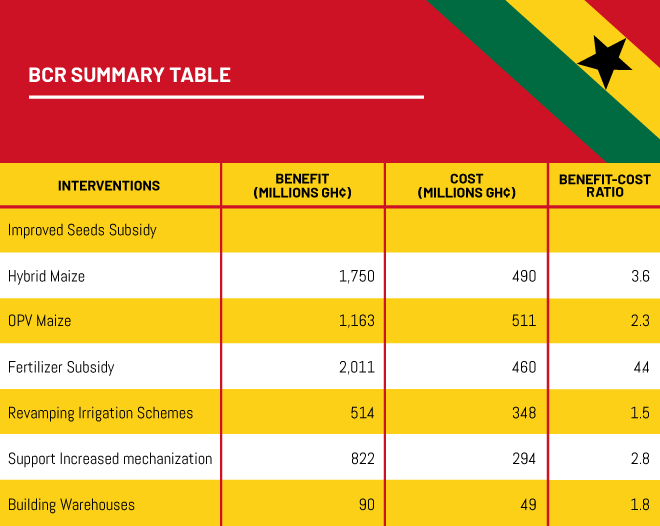

Our results show that all the interventions had a BCR value of greater than 1, implying positive returns to the investments. The most promising interventions were subsidising hybrid seeds and fertilizer. These had higher BCRs of 3.6 and 4.4 respectively at an 8% discount rate. This was followed by mechanisation programme (2.8), OPV seeds (2.3), the warehousing intervention (1.8) and the irrigation intervention (1.5) in that order. We suggest not putting too much weight on the absolute magnitudes due to inherent uncertainties in the analyses, and only some weight on the relative BCRs. That said, it appears that encouraging farmers to use hybrid and fertilizer inputs via subsidies would be more efficient than other interventions. The greatest source of uncertainty, and the one that would change the policy implications the most is the assumed extent and waste associated with smuggling of subsidized seed and fertilizer, particularly the latter. We have attempted to account for these in our analysis using actual expenditure data from government sources. The study concludes by noting that even though these individual interventions do all have positive returns, the very nature of agriculture means that complementarities could result in returns that will be much higher than the sum of the individual returns suggest.

Intervention I – Subsidising Improved Seeds

Overview

For various reasons, many smallholder farmers in Ghana do not use improved seeds, which are not only more resilient but also provide higher yields. There are four principal factors that contribute to the low uptake of improved seeds. First, knowledge of hybrid varieties among farmers seems to be low. Second, even with knowledge of these varieties, farmers may be too risk averse to try a new technology. Third is the cost, particularly of hybrid varieties. Fourth, is the issue of access. Farmers who may be able to afford are not always able to procure them when they are needed. This is partly due to limited production of certified seeds resulting from a lack of a guaranteed market. Subsidizing improved seeds for smallholder farmers has the potential to address all of these issues either directly (reducing the cost) or indirectly (via decreasing the costs of learning about seeds, improving the demand to stimulate increased production). Increased uptake of improved seeds can increase yields and therefore farmer welfare.

Implementation Considerations

This intervention considers a subsidy on improved maize seeds for both hybrids and OPVs. We focus on maize because it is probably the most popular crop among smallholder farmers and accounts for the highest portion of agricultural land in Ghana. Additionally, improved maize seeds are the most prominent within the seed industry in Ghana. The proposed intervention is for government to continue to provide a subsidy of 50 percent on maize seeds until 2023, reduce the rate to 40 percent in 2024, 30 percent in 2025 and then decrease the rate to zero by 2028. By then, it is hoped, farmers would have observed that the benefits of using certified seeds outweigh the cost and continue using them. The analysis models the impact for a further five years, even when there is no subsidy, to capture these learning gains. The benefits and costs are measured against a scenario where there are no subsidies.

Without persuasion, farmers may not adopt improved seeds for the reasons mentioned above. These risks can be mitigated if government extension agents are a key part of the intervention to demonstrate and ensure farmers appropriately used new seeds and generate the expected yield increases.

Benefit and Cost Estimations

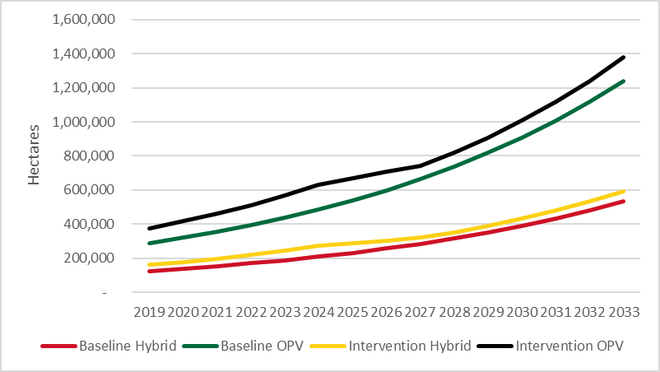

We assume farmers would respond to the lower price of seeds by increasing their use of certified seeds without necessarily increasing total land area of plantations. The estimated use of hybrid and OPV seeds are depicted in Figure 1 for both the intervention and baseline cases. A 50% subsidy boosts the use of seeds by 30%.

Figure 1: Use of improved seed (OPV and Hybrids) - baseline and intervention

The costs of extending the subsidy on improved seeds include the financial outlay of government and the extra costs to farmers, which increase as the subsidy is gradually removed. The public cost of the maize seeds subsidy is based on the budgeted expenditures, as reported by MoFA in the Planting for Food and Jobs documents (MOFA, 2017b), and covers payment for the 50 percent subsidy on the seeds, expenditures for training, publicity, dealing with seeds producers and leakage. Switching from local to improved seeds would also increase fertilizer, labour and transport costs for farmers. The cost of the intervention is GHS 490 million for subsidizing hybrid seeds and GHS 511 million for subsidizing OPV seeds over 15 years. Unsurprisingly, the actual seeds make up most (~80%) of the cost during the subsidy regime. During the five-year period after the subsidy is removed, seeds only make up 50% of the marginal cost.

The primary benefit of the intervention is higher agricultural yields, but this depends on the extent of uptake by smallholder farmers. Based on existing literature, we assume that hybrid seeds increase yield by 2.0 MT / ha, while OPV seeds increase yields by 0.51 MT / ha. The value of increased output averages GHS 156m and 92m per year for hybrid and OPV respectively. An additional benefit is the value of the subsidy for farmers who would have bought seeds without the subsidy. This value averages 36 m for hybrids and 42m for OPV per year.

In total, farmers switching from local seeds to using hybrid seeds generate estimated benefits of GHS 1,750 million as compared to an additional cost of GHS 490 million, assuming an 8 percent discount rate. The BCR is 3.6. If instead OPVs are adopted in place of the local seeds, the estimated benefits would be GHS 1,162 million and the additional cost would be GHS 511 million, resulting in a benefit cost ratio of 2.3. From these results, subsidizing improved seeds would provide net benefits to farmers and to the country.

Intervention II - Fertilizer Subsidies

Overview

The Ministry of Food and Agriculture (MOFA) has reported fertilizer use per hectare among smallholder farmers is between 13kg and 15kg (MoFA 2019). This is far below the optimal level for many crops. The costs associated with fertilizer use have been identified as one of the reasons for its low uptake. Therefore, one way of increasing fertilizer intensity is to reduce the price of fertilizer so farmers can afford the required quantities as reported by Imoru and Ayamga (2015). This intervention examines the viability of a programme that maintains the current 50% subsidy for a period of 5 years with a gradual removal over 5 years back to 26%. An alternative scenario was also built for when the subsidy is completely taken off at 0%. These analyses are compared to a case where subsidies remain at 26%.

Implementation Considerations

We assume the subsidies will be maintained at 50% over a period of 5 years. From the 6th year, it will be gradually reduced to 45%, then to 40%, 36%, 31% and finally reach 26% by 2028. We analyse benefits for five years after the subsidy is removed / lowered to account for medium impacts of learning.

The main risk with respect to fertilizer subsidies is smuggling. This has and remains a concern of policy and rightly so. The cost to smuggling has also been modelled into the analysis and is estimated at 2.6% of the government’s cost based on government provided data.

Benefits and Costs Estimations

The intervention is expected to boost the use of fertilizer, with the expected change differing by crop. The main assumptions are below:

| Crop | Price elasticity to fertilizer use | Elasticity of crop yield to fertilizer use | Elasticity of crop yield to fertilizer price | Actual fertilizer use (kg/ha) | Recommended use (kg/ha) |

|---|---|---|---|---|---|

| Yam | -0.83 | 0.00065 | -0.011 | 10.00 | 110.00 |

| Maize | -0.83 | 0.00814 | -0.209 | 40.00 | 141.30 |

| Cocoa | -0.83 | 0.00223 | -0.816 | 15.00 | 187.50 |

| Pineapple | -0.83 | 0.041 | -0.107 | 15.00 | 237.50 |

In general, fertilizer use increases by 27% initially, and decreases as the subsidy is lowered.

The key cost elements of this intervention include the financial outlay of the subsidy, administrative/transportation, and leakage (smuggling) costs. There is also the cost to farmers as a result of the use of more fertilizers than they would have otherwise used.

In terms of benefits, it is envisaged that the subsidy will increase fertilizer use by farmers and subsequently improve the yields of crops. Additionally, the reduction in price of fertilizer for the farmers who would have used fertilizer without the subsidy is a benefit.

Over the period 2019 to 2033, the total benefits of the fertilizer subsidy in present value terms is estimated to be GHS 2,011 millions, at a discount rate of 8%. The costs amount to GHS 460 million. We observe that the cash crops, cocoa (BCR = 5) and pineapple (BCR = 20) respond highly to the intervention compared to staple crops (maize; 3.97 and yam; 0.93). The overall BCR is 4.4, and results suggest that at any discount rate, the fertilizer subsidy intervention will engender benefits that will be around 4 times more than the cost. The alternative scenario, reducing subsidy to 0% at the terminal period equally showed positive BCR values indicating the viability of the intervention at all levels.

In all these, private sector players who are the main importers and distributors of the fertilizer stand to benefit from the guaranteed market. However, if inefficiencies resulting from delayed payment by the government persist, it could crowd out their investments.

Since the assumption is that farmers could be weaned off the subsidy subsequently, it is imperative that other accompanying measures come together with the intervention, such as building the capacity of farmers, helping them to better access credit and expanding market access and structures. This will incentivize farmers to increase productivity by adopting best practices including optimal fertilizer application which hitherto has been motivated due to the intervention.

Intervention III - Irrigation

Overview

The effects of climate change continue to aggravate the plight of farmers in Sub-Saharan Africa. The scarcity of water and irregularity of rainfall has been a restraining factor for crop production in Sub-Saharan Africa, and Ghana is not an exception. Public investment in irrigation development in Ghana has declined considerably from the 1990s, and there is increasing uncertainty about the returns to these vast investments (Namara et al., 2011). Previous experience saw public irrigation initiatives stalled due to machinery breakdowns, high electricity costs, old and choked canals and poor service repayments. More recently, there is renewed effort by government to rehabilitate some existing irrigation schemes, leading to some of the abandoned schemes being brought back to production (Akrofi et al., 2019).

This intervention proposes to rehabilitate the following already existing irrigation schemes: Ashaiman, Dawhenya, Weija, Afife, Aveyime, Mankessim, Okyereko, Subinja, Sasta and Akumadan. Even though these are part of the Ministry’s long-term plans, they are yet to be implemented. The total area to be covered by these 10 irrigation sites is 3,443 hectares. The rehabilitation of these irrigation schemes covers a period of 30 months as compared to 18 months proposed by the Government for the other schemes. This is to cater for unforeseen challenges that may arise during the implementation phases; including institutional changes that are needed to make the Water Users Association (WUA) effective with governance and the collection of user fees. The performance of smallholder farmers’ engagement in irrigation water management in the past has been poor and there have been several instances of default payments (Namara et al., 2011). Hence the intervention includes a mechanism that allows farmers flexible payment so that they are more likely to access the facilities.

Implementation Considerations

For this intervention, ten sites will be rehabilitated over a period of 30 months. The key crops to be grown in these areas include rice, pepper, okra and tomatoes. The intervention assumes that government covers the cost of rehabilitation, while the cost of ongoing maintenance is borne by farmers in the form of user fees. Based on stakeholder interviews, this service fee is about GHS 200 per acre annually (approximately GHS 500 / US$ 91 per hectare).

The schemes will imitate the management structure of existing irrigation schemes being handled by private sector under the regulation of the GIDA. The new operation and management model is envisaged to mitigate the problem of recurrent expenditure incurred by Government, almost every decade, on irrigation management in the country. It will ensure that the only burden on the government will be to repair the main canals every 30 years as there would be enough money generated by the various schemes to maintain the secondary and tertiary canals (Bokpe, 2017).

The institutional changes required to enable this intervention are a source of risk, given known challenges with this type of intervention in developing countries, including Ghana. However, this appears to have been mitigated to some extent with GCAP project – as previously mentioned, a similar initiative to the one described here. According to Koomson (2020), the project which involves the digitization of the Kpong Left Bank Irrigation scheme with an automation system is already about 63% complete.

There are two additional sources of uncertainty that one anticipates with this intervention. The first relates to the pricing of the water which will be done per litre as opposed to what has been done in the past – which was per hectare. A second source of uncertainty is the fact that the scheme will be under private management even though oversight will be by GIDA, as described earlier. Given that farmers are used to the old system, one anticipates some level of apprehension and possible cooperation issues from the farmers initially. This calls for education and sensitization of farmers on the operation of the new system.

Benefits and costs Estimations

The key benefit for this intervention is increased yields. The increase in yield will come from 2 main sources. First the increase due to the more efficient use of nutrients by the plants in the presence of water – here there is increased yield over a production cycle, assumed to be 20%. The second source of the increase is due to the fact that with irrigation, a farmer can have two production cycles in a year. In that case the annualized yield also increases. In this report we assume the annualized yield increases by 100% - i.e. farmers can undertake 2 times production instead of the 1. The benefits are estimated at GHS 514m over a 10 year period.

The implementation of the irrigation rehabilitation programme would have two major cost components. These are rehabilitation costs and maintenance costs. The government would bear the cost of rehabilitation of the irrigation schemes. The cost of rehabilitating an irrigation site is about GHS 104,000 (US$ 20,000) per hectare. Given a size of 3,443 hectares, the the total cost amounts to GHS 360 million (US$69 million), spread over three years.

To ensure longevity and sustainability of the irrigation schemes, the farmers (beneficiaries) would be charged additionally, service fees to maintain the various irrigation schemes. Information was obtained from discussions with a member of the management team of Irrigation Company of Upper Regions (ICOUR) Ghana on the maintenance cost (service and operation charges) of irrigation schemes. Based on that data we note that farmers are charged a service fee of about GHS 200 per acre annually. This amounts to about GHS 500 (US$ 91) per hectare. Maintenance costs after rehabilitation are approximately GHS 2m per year.

By 2030 the total cost of this intervention, discounted at 8% is estimated to be GHS 348 million

Intervention IV – Mechanisation

Overview

Mechanization, particularly access to tractor services, is essential for expanding agriculture as well as improving productivity of the existing farms. Unfortunately, the use of mechanization or tractor services by smallholder farmers remains low in Ghana. Part of the reason is lack of the services in many farming communities. In other places where they exist, costs have been a limiting factor. MoFA estimates that out of the potential merchandisable agricultural land of about eight million hectares, only 2.4 million hectares-representing about 30 percent, are under mechanization. This intervention proposes to increase area under mechanization by 13 percent in the next 10 years through purchasing of additional tractors and implements. Here we expect it to lead to improvements in soil quality (soil moisture, water retention, air circulation, etc.) and thereby result in higher plant growth and development - increased yields.

Implementation Considerations

Our estimation is based on parameters relating to maize. However, we believe this can be extrapolated to other crops such as rice, yams, and cowpea as well. Indeed, other studies based on other crops also show increases in yields as a result of the mechanization (see Osei 2013). We assume that yield will increase by 11% as a result of the mechanization (see Benin et al 2011). Additionally, we assume that more area will be brought under cultivation as a result of the increased use of tractors.

We expect mechanisation to increase by 13% over the next 10 years. This will be over and above what government plans under AMSEC. Our model estimates the costs and benefits stream over the period 2020 to 2039 to ensure all benefits are captured over the useful life of the tractors (the final tractors bought in 2030 will only cease operating in 2039).

One of the key risks has to do with the efficacy of the intervention in delivering the tractors to the right sections of the private sector so as to ensure efficiency of use. Note that one could envisage a situation where the spending on the tractors will be made but there may not be used for their intended purpose, for example due to lack of maintenance.

Benefits and Costs Estimations

The study takes into consideration several cost elements of mechanization. Based on Hossou et. al. (2016) there are many cost components including the purchase of tractor and implements, repairs and maintenance, fuel, insurance and business registration, building of sheds to house the tractors, overheads including depreciation, lubricants, oil, among others.. The total cost of increasing the area under mechanization for this intervention amount to GHS 294 million in present value terms with capital expenditure making up around 4/5th of the cost.

Three main benefit of the intervention is an increase in yield, assumed to be 11% based on available evidence. This leads to an output increase of around 0.2 tonnes per ha. The benefit is estimated at GHS 822 million over the period 2020-2039 (using an 8% discount rate).

The BCR is 2.8.

Intervention V – Building of Warehouses

Overview

A World Bank report disclosed that in Sub-Saharan Africa (SSA), a large amount of food produced (particularly grains), is lost after harvest with an estimated value of US$ 4 billion (World Bank, 2011). For this reason, investing in post-harvest loss reduction is potentially a smart and impactful intervention to ensure food security (GIZ, 2013a). The narrative on post-harvest losses in Ghana is no different. Ansah and Tetteh (2016) recognize the need to reduce post-harvest losses as an essential means of improving food security in the country and one way to minimize post-harvest losses is to manage storage losses. It is expected that when post-harvest storage losses are well managed, farmers will be able to keep their produce for a long time without significant losses, and will be able to sell at good and attractive market prices. Also for subsistence farmers, minimizing post-harvest losses is a way of making sure food is available all year round (Ansah et al., 2018). Hence a reduction in post-harvest losses provides a significant pathway of reducing poverty and improving nutrition.

Because of the risks associated with grain storage, farmers try to minimize losses by selling their grain soon after harvest, leading to low market prices as the markets are flooded with freshly harvested grains (Opit et al. 2014). Conversely during the off-season, the price of maize is usually highest as maize is not easily available. According to Bruce (2016), Ghana loses about 318,514 tonnes of maize annually to post-harvest losses. This figure represents about 18% of the country’s annual maize production. Therefore, improving food security particularly for the poor, cannot be accomplished without sufficient maize storage so as to stabilize prices during the off-season. Also, maize could become an economically important export commodity for the country if excess maize produced is stored.

Implementation Considerations

The intervention will look at constructing 46 new warehouses with an average capacity of 1,000 tonnes for the next 3 years. These new warehouses will supplement government’s effort in curbing post-harvest storage losses. It must be noted that even with the proposed intervention of additional warehouses, only a small fraction of the post-harvest losses will be addressed. Specifically, the proposed intervention will start with 20 warehouses in 2020. An additional 20 warehouses will be constructed in 2021 and thereafter 6 warehouses will be built in 2023. The capacity of warehouses to be built will be 1,000 tonnes each. It is assumed that postharvest losses which is currently estimated to be about 18% will reduce to about 5% for the maize output that is stored in these warehouses.

Benefits and Costs Estimations

The benefit of this intervention is the value of post-harvest losses avoided. There is an additional benefit in terms of stability and reduction of prices over time (reduction in prices was computed on an annual basis) but this was not estimated in this analysis. In terms of modelling, we essentially capture and value the benefits as a reduction in post-harvest losses associated with the building these 46 warehouses by 2029. As stated earlier, post-harvest losses amount to about 18%. Some studies have found that using scientific methods can reduce grain losses to as low as 2% (Kumar and Kalita, 2017). For our modelling we will assume that the losses will reduce from the 18% to about 5% with the warehouse intervention. This figure makes room for inefficiencies that are still inherent in the storage system. Given that each warehouse can hold 1000 tonnes, the expected post-harvest storage loss avoided is around 6,000 tonnes per year in steady state.

Applying a value per tonne of $370 per tonne, and decreasing 1.2% per year to account for increased supply arising from the intervention, the total benefits for the 15 years of the project life amount to GHS 90 million, using a discount rate of 8%.

The implementation of the intervention will have a number of key cost items. These will include the cost of constructing the warehouses, maintenance cost, handling and administrative cost, warehousing insurance as well as the cost of employing caretakers, aggregators and sub-aggregators. The most important cost assumptions include is the unit cost of a new warehouse estimated at GHS 460,000.00. This estimate was obtained from government’s document on Planting for Food and Jobs (MoFA, 2017) and is consistent with that used in Government’s budget allocation for the Planting for Food and Jobs Programme (PFJ). By Year 3 when all the 46 warehouses have been built the total cost of the intervention will amount to GHS 6.5 million for that year. For the entire 15 years, which we assume will be the life of the project, the present value of the total costs is obtained as GHS 49 million, using a discount rate of 8%. The BCR is 1.8.